Participating interest rate swap

Summary

A participating interest rate swap is a derivative instrument that combines an interest rate swap with an interest rate cap. A portion of the debt is hedged with a swap and the remainder with a cap.What is a participating swap?

A participating interest rate swap is a derivative instrument that combines an interest rate swap with an interest rate cap. A portion of the debt is hedged with a swap and the remainder with a cap. The degree of participation is determined by the proportion attributable to the cap. The cap premium is embedded in the swap rate eliminating the cost. The embedded swap rate and the cap strike rate are set at the same level.

Objective

The purpose of such a hedge is to provide the borrower with protection against rising short-term interest rates and the ability to benefit from a drop in rates.

How does it work?

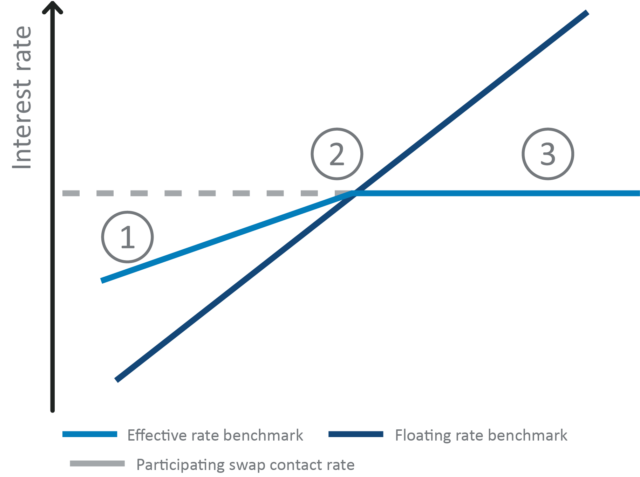

On the reset date, if the floating rate (for example three-month LIBOR) is below the strike rate, then the borrower will pay the fixed rate of interest in return for a floating rate of interest on the portion covered by the swap. On the capped portion, the borrower will pay the floating rate subject to a maximum determined by the cap. If the floating rate is above the strike rate, the borrower receives the difference between the fixed rate and the floating rate on both the swapped and capped portions of the debt, establishing a maximum cost of funds at the strike rate of the participating swap.

Two scenarios of where the floating rate could settle and what the borrower will need to pay when using a participating swap.

Advantages

- The borrower receives the comfort of a known maximum rate of interest on 100% of the hedged debt

- The borrower can benefit from lower floating rates

- The strategy provides the borrower with greater flexibility in managing cash flows

- There is no upfront premium

Disadvantages

- A participating swap rate will be higher than the market swap rate

- If the floating rate fails to rise above the cap strike rate during the tenor of the cap, the borrower may feel they received no value

- Potential termination costs are payable on the swapped portion of the debt should the hedge be terminated early in a low rate environment

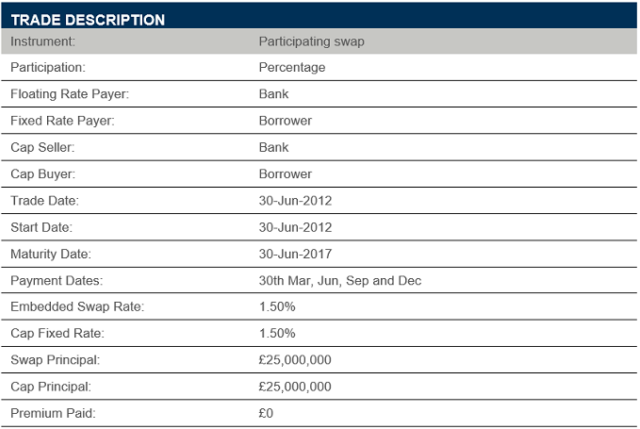

A description of what a participating interest rate swap trade could look like in practice.

Participating interest rate swap graph showing three potential outcomes over time.

Ready to have weekly rates and capital markets insights delivered to your inbox?

Subscribe for industry insights

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

Transactions in over-the-counter derivatives (or “swaps”) have significant risks, including, but not limited to, substantial risk of loss. You should consult your own business, legal, tax and accounting advisers with respect to proposed swap transaction and you should refrain from entering into any swap transaction unless you have fully understood the terms and risks of the transaction, including the extent of your potential risk of loss. This material has been prepared by a sales or trading employee or agent of Chatham Hedging Advisors and could be deemed a solicitation for entering into a derivatives transaction. This material is not a research report prepared by Chatham Hedging Advisors. If you are not an experienced user of the derivatives markets, capable of making independent trading decisions, then you should not rely solely on this communication in making trading decisions. All rights reserved.

20-0286